The electoral surprise triggered a sharp shiftin expectations for Argentina, driving a clearly more favorable political and economic outlook. The administration’s strong performance —securing more than 41% of the vote and defeating Peronism by over 10 percentage points, including an unexpected win in Buenos Aires Province, where it had lost by more than 14 points just two months ago— significantly strengthens the Government’s position in Congress and improves the prospects for effective governance. This outcome redefines the political landscape, providing a more solid foundation to advance structural reforms and consolidate the economic policy path.

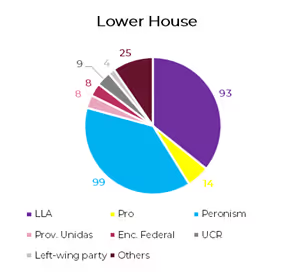

This new political balance will not only enhance the Executive’s governability —with its own veto power and greater negotiating leverage— but also bring it closer to the majorities required to push forward key structural reforms. Specifically, the administration will hold 93 seats in the Lower House (107 including allies) and 20 seats in the Upper House (26 with allies).

The election outcome triggered an immediate and decisive market reaction. On the Monday following the vote, markets saw a historic rally across both bonds and equities. Sovereign USD-denominated debt surged an average of 19%, bringing the country risk toward 700 bps, while the Merval jumped 31% in dollar terms—its largest single-day gain since the restructuring. At the same time, ARS-denominated curves strengthened noticeably, reflecting the sharp shift in expectations following the electoral result.

From our perspective, local assets still offer meaningful upside, prompting a shift from a defensive to a more offensive stance. This adjustment reflects the consolidation of a more constructive baseline scenario following the electoral shock, supported by three key pillars:

1. Fiscal commitment. The Government remains firmly focused on achieving a balanced fiscal position, a goal now reinforced by a Congress more inclined to support consolidation measures, strengthening the sustainability of the economic program.

2. Governability. The new legislative balance provides a stronger political foundation, enhancing the Executive’s ability to advance structural reforms and sustain the economic stabilization process, thereby reducing uncertainty and reinforcing market confidence.

3. Reserve accumulation. The external front remains the weakest pillar, though with room for improvement. Markets are looking for a concrete FX-accumulation strategy that could combine Treasury purchases in the FX market, new debt issuance, or both—supported by U.S. financial backing through the USD 20 billion swap line and the potential implementation of repo operations with private banks.

Viewed as a whole, these pillars shape a more robust backdrop for the economic program and reinforce the perception of short-and medium-term stability. The path toward an earlier-than-expected reopening of capital markets now looks considerably clearer, prompting a shift inpositioning toward a more constructive strategy.

USD-DENOMINATED DEBT STRATEGIES

In the current environment, sovereign USD-denominated bonds continue to show meaningful room for further spread compression. In January, the GD35 was yielding 10.5%, of which 4.8% reflected the risk-free rate (UST10Y) and 4.2% the average LatAm risk premium, leaving a local spread of roughly 150 bps attributable exclusively to Argentina-specific risk. Today, with the risk-free rate at 4.0%, the LatAm premium at 3.3%, and Argentina’s country risk at 693 bps (implying a 10.9% YTM), that local premium has widened to about 365 bps—more than double the level recorded at the start of the year.

This suggests that Argentina still has close to 215 bps of “pure” local spread to recover merely to return to January levels, while full convergence toward regional benchmarks would imply potential tightening of up to 365 bps. Despite the recent appreciation, Argentine sovereigns continue to trade at a significant premium to LatAm peers, leaving scope for additional upside if the new political and economic backdrop continues to consolidate.

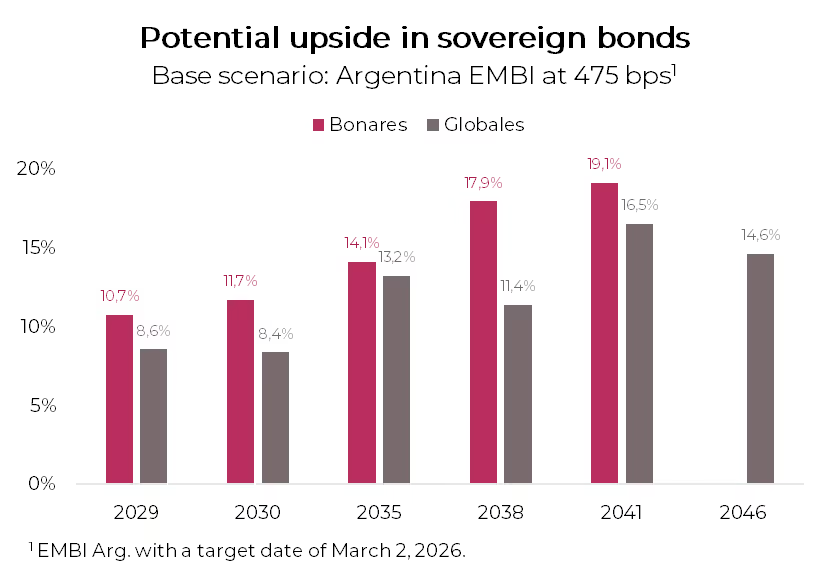

In this context, our base case envisions roughly 215 bps of country-risk compression —bringing spreads toward the 475bps area by the first quarter of 2026— which would pave the way for a reopening of access to international capital markets. Against this backdrop, sovereign bonds under local law stand out as the instruments best positioned to capture that adjustment. In particular, we highlight the AE38 (13% YTM), which offers an estimated upside of 17.9%, while among the ARGENT bonds (Globales) we favorthe GD41 (11% YTM) given its higher potential upside of 16.5% and its superior liquidity.

On the other hand, BCRA-issued debt also shows room for further repricing in this new environment. The Bopreal Series 4-A (BOA8D) offers a 15.8% YTM, above the 12.7% currently available on the AL30,with only a slightly longer duration. As an instrument issued by the Central Bank, its credit risk is lower than that of Treasury debt, while the relatively small outstanding amount (USD 845 M) and the option to use it for tax payments starting in April 2028 further enhance its relative appeal.

ARS-DENOMINATED DEBT STRATEGIES

While the momentum in hard-currency debt is undeniable, the external front remains the most fragile element of the macro framework. This is reflected not only in the balance of payments but also in market-implied expectations, which continue to price an exchange rate above the upper bound of the FX band—particularly evident in FX futures from December onward. Both the official exchange rate and financial dollars show that demand for hedging remains firm, even after the post-election rally in ARS-denominated curves.

In this regard, we continue to argue that the Government should recalibrate the FX band, setting a lower limit more aligned with the current level of the exchange rate. This would allow the BCRA or the Treasury to repurchase foreign currency and streng then international reserves, addressing the main vulnerability of the current economic program.

Under this scenario, we continue to prioritize hedging strategies through dollar-linked instruments. In particular, we highlight the dollar-linked TZVD5 (devaluation +21%) and the D16E6 (devaluation+12%), which imply a devaluation at maturity of 2.3% and 4%, respectively—levels that appear meaningfully below our projections.

On the other hand, we expect interest rates to begin declining, while inflation could take somewhat longer to ease due to greater FX tensions, albeit with a limited pass-through. This dynamic would reduce real rates and, in turn, provide renewed support for CER-linked bonds, which would regain relevance as a defensive hedge within the ARS universe. Within this segment, we highlight the TZX26 (CER +12%), which embeds an average breakeven inflation of 1.5% m/m between October 2025 and April 2026.

Dual bonds are once again emerging as an attractive alternative within ARS-denominated instruments. Although interestrates should begin a downward path, the breakeven TAMAR rate—the rate that equates the direct yield of a fixed-rate instrument with that of a dual bond of similar duration—remains well below the current TAMAR. In this respect, the TTM26 (TAMAR +5.1%) and TTJ26 (TAMAR +6.8%) look particularly appealing: their breakeven TAMAR rates stand at 18.3% and 22.5%, respectively, compared with the current TAMAR of 45.94% NAR. This means rates would need to drop sharply forthese instruments to stop outperforming their fixed-rate alternatives.

For more aggressive profiles, the Bonte 2030 (29.8% NAR) stands out as an attractive option for longer-horizon carry trade strategies, offering competitive dollar returns even under demanding exchange-rate assumptions. In a conservative scenario with rates declining to 20% NAR over the next 12 months, the bond would deliver a potential return of 9.6% in dollars at an exchange rate of ARS 2,000 and 21.7% at ARS 1,800,excluding coupon reinvestment. If rates remain at current levels, the downside would be 6.5% with an exchange rate of ARS 2,000 and 4% at ARS 1,800. In this context, the risk of holding ARS positions increases as the compensating spread for FX risk narrows.