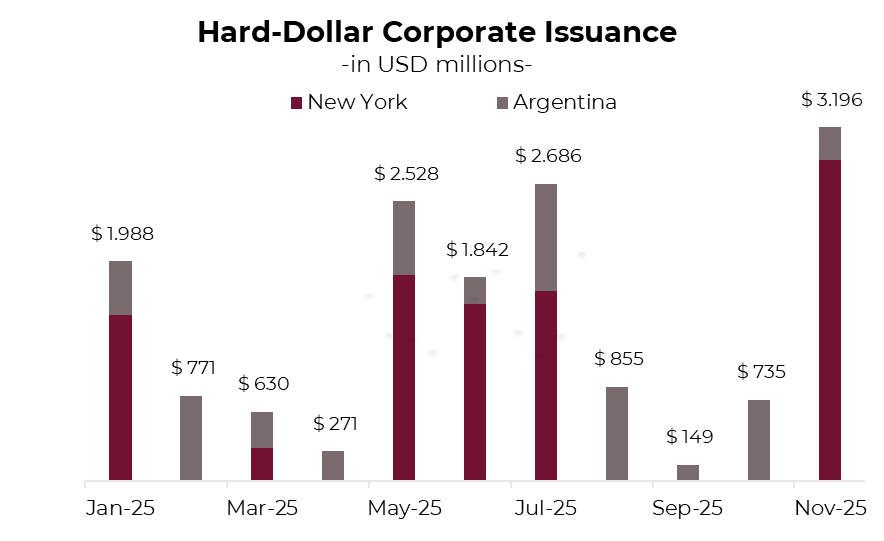

With political uncertainty now behind us, financial conditions have shown a sustained improvement, reflected in country risk falling 480 bps to the ~600 bps area. This has encouraged corporates —and, to a lesser extent, provinces— to re-enter financial markets, placing more than USD 4.000 M in debt across international and local markets.

Against this backdrop, companies issued nearly USD 1.900 M in bonds over the past week: Pampa (USD 450 M due2037, 7.75%), Pluspetrol (USD 500 M due 2031, 8.38%), TGS (USD 500 M due 2035,7.75%) and Edenor (USD 204 M due 2030, 9.75%) under New York law, while Galicia (USD 144 M due 2026, 6.00%) and Banco Patagonia (USD 47 M due 2026, 6.25%) completed local-law issuances alongside Banco Hipotecario and Credicuotas. With these deals, November corporate issuance already totals USD 3.200 M —of which USD 2.900 M are under foreign law— in addition to CABA’s recent USD 600 M placement at an 8.125% yield and a 7.8% coupon. The financing calendar will remain active in the coming days: CGC aims to issue up to USD 500 M in 5-year bonds in international markets, while Genneia plans to place up to USD 300 M inmaturities ranging from 5 to 8 years. If both transactions price within the targeted amounts, total November issuance —including corporate and provincial placements— could exceed USD 4.500 M.

USD-DENOMINATED STRATEGIES

This stronger flow through the financial channel comes at a time when sovereign hard-currency debt has already delivered a substantial post-election rally, with yields compressing from 16%to 8.3% on the short end and from 14.5% to 9.8% on the long end of the Global curve. In this context, while sovereigns may still have some upside left, the latest corporate and provincial issuances are beginning to emerge as compelling alternatives to diversify risk and capture still-elevated spreads —particularly in a market showing signs of normalization and where the credit fundamentals of several private and sub-sovereign issuers remain solid.

At the same time, the corporate universe is gaining prominence not only due to the competitive YTMs seen inrecent placements —particularly under foreign law— but also because of its relatively greater stability: these instruments pay higher coupons than sovereigns, offer more attractive current yields, and tend to exhibit lower volatility and less sensitivity to local political-economic risk. In a context where the sovereign curve has already absorbed much of the recent rally, corporate bonds are beginning to gain traction as an appealing alternative within USD-denominated strategies.

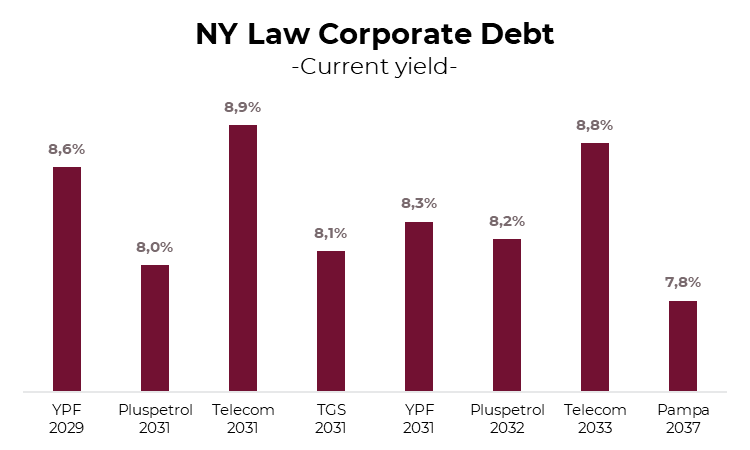

We highlight credits from issuers such as YPF, Pluspetrol, Loma Negra —rated AAA— and Telecom —rated AA+— which continue to offer solid profiles and competitive returns within the corporate segment. Within the foreign-law universe, we see value in YPF 2029 YMCIO (6.6%YTM), YPF 2031 YMCXO (7.5% YTM), and Telecom 2033 TLCPO (8.3% YTM), with current yields in the 8.3%–8.6% range depending on the instrument. Pluspetrol’s new 2032 issuance (8.0% YTM) also screens well, offering a current yield of 8.2%.

Within the local-law universe, Loma Negra 2027 LOC5O (7.3% YTM), YPF 2028 YMCZO, and Telecom 2028 TLCOO (7.4% YTM)stand out, with current yields ranging from 6.9% to 7.9%.

Regarding sub-sovereign debt, the new CABA 2033 issuance, with a 7.8% coupon, is already showing indicative quotes above its launch price of 98.295 and is emerging as an attractive alternative given its lower relative risk compared with the sovereign. Added to this is Córdoba 2032 (CO32), which trades around an 8.1% YTM and —similar to CABA— maintains a moderate debt burden relative to its revenues and a financial balance that, although it weakened in the first half of 2025 compared with the same period in 2024, continues to reflect a solid fiscal position.

ARS-DENOMINATED STRATEGIES

Dual bonds

We consider Dual bonds, together with CER-linked instruments, to remain the most attractive alternatives for capturing higher returns. Looking ahead to the coming months, the Treasury faces sizeable maturities —ARS 14 trillion in November and ARS 40 trillion in December— in a context where ARS deposits at the BCRA remain low (ARS 4.7 trillion). This mismatch between financing needs and available liquidity suggests that rates have likely found a floor and could remain stable or even show a slightly upward bias.

Under this scenario, the TAMAR ratemay stabilize around current levels of 33% NAR, enhancing the relative appeal of Dual bonds. When assessing the TAMAR breakeven —the level at which an investor is indifferent between a fixed-rate bond and a Dual— we observe that it remains below our projections for the March and June maturities. In this context, we prioritize TTM26 (TAMAR +0.3%) and TTJ26 (TAMAR +0.8%), whose TAMAR breakeven levels stand at 19.9% and 27.3%, respectively.

Inflation linked bonds

Regarding inflation-linked debt, we see value in shortening duration. Over the past two months, inflation has struggled to fall below 2.0% m/m, and we expect this pattern to persist due to pressures from seasonal factors, regulated prices, and food —particularly beef—which will continue to limit a more pronounced disinflation in the near term.

In this context, the short end ofthe CER curve becomes more attractive when comparing breakeven inflation against our projections, which anticipate a more persistent inflation path than the one implied by market pricing. The market is currently expecting average inflation of 1.9% m/m between November and January, and 1.6% m/m between February and April. Under a scenario where inflation remains above 2.0% m/m through the first quarter of 2026, the best-positioned instruments within the CER segment are TZXM6 (CER +5.8%) and TZX26 (CER +6.3%).

Fixed-rate securities

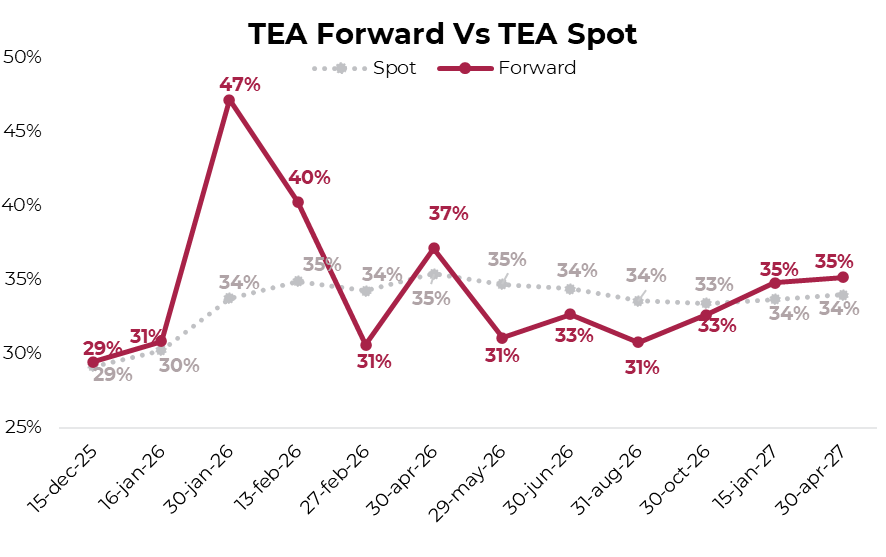

Regarding the fixed-rate curve, and considering the recent compression in ARS yields, the question of whether it is convenient to extend duration has resurfaced. To evaluate this decision, werely on forward rates, which allow us to identify the indifference yield between two strategies: investing in a short-term bill and reinvesting principal and interest at maturity, or positioning from the outset in alonger-term instrument. If, at the time of reinvestment, the spot rate of the long bond stands below its forward rate, taking the long bond initially would have been more efficient; if it is above, the optimal choice is to invest inthe short-term bill and subsequently reinvest in the longer segment.

The analysis highlights a specific point of relative value within the fixed-rate curve. The Boncap T30E6 (36% YTM) shows a forward rate close to 47%, implying that, upon maturity of the S16E6 (30% YTM), the long bond would need to trade at that yield to match the strategy of first investing in the short bill and then reinvesting. A similar conclusion emerges when comparing it with the December LECAP (T15D5), whose forward rate stands around 40%.

These implied yield levels forJanuary appear elevated under our assumptions —particularly in a scenario where rates may prove resistant to further declines— which reinforces the case for remaining positioned in the short end of the fixed-rate curve and reinvestingat maturity. In this context, T30E6 appears as a tactical opportunity within the short-term space, with no clear premium for extending duration toward longer maturities.

Dollar-linked bonds

Regarding FX hedging, we maintain our position in the January 2026 segment. The government faces the need to rebuild reserves in order to move toward the target agreed with the IMF —net reserves around USD -3.500 M by December, compared with a current level near USD -10.000 M— a goal that appears highly demanding under present conditions. Even so, making progress in that direction and sending a credible signal of commitment to the market —crucial for facilitating potential market access— would require recalibrating the exchange-rate band framework by establishing a floor more aligned with the current level of the official FX rate, allowing the BCRA to purchase foreign currency and rebuild international reserves.

In this context, we consider it appropriate to maintain hedging through the D16E6 (Devaluation +0.96%), which is pricing in an increase in the official exchange rate of only 3.5%, below our projections.

.avif)