Executive summary

Argentina’s economy is stabilizing after years of volatility, driven by bold structural reforms. The new administration has tackled deep-rooted fiscal, monetary, and exchange rate issues, laying the foundation for sustainable growth. Despite holding world-class lithium, shale gas, and agricultural resources, decades of mismanagement had constrained Argentina’s potential.

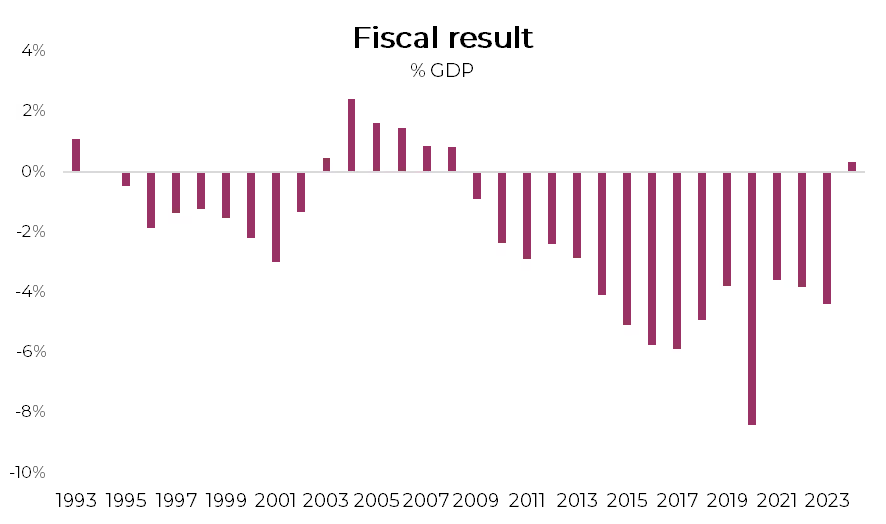

The fiscal adjustment has been unprecedented, delivering a historic surplus. In 2024, the government achieved a fiscal surplus of 0.3% of GDP, reversing a 4.4% deficit in 2023. The adjustment, focused on reducing public spending and limiting Central Bank financing, has anchored inflation expectations and provided stability.

Inflation has decelerated sharply but remains a priority. From a peak of 211% y/y in December 2023, inflation dropped to 118% by year-end 2024 and is projected to reach 24% by December 2025. Lower inflation has driven real income recovery, reducing poverty from 54% to 38%, and remains central to maintaining public support.

The economy is recovering from the 2024 recession, with a strong growth outlook for 2025. After contracting 2.3% in 2024, real GDP is expected to grow 5% in 2025, supported by agricultural exports, energy, and an improving domestic market. While the recovery is uneven, key sectors like mining and agriculture are driving a rapid rebound.

Exchange rate policy and capital controls are the primary risks. The administration has prioritized exchange rate stability to reinforce disinflation, but real appreciation has eroded competitiveness. While an agreement with the IMF and the removal of capital controls are on investors’ radar, such moves are unlikely before the 2025 legislative elections.

The political landscape remains pivotal for advancing reforms. Despite initial challenges due to limited representation in Congress, the administration has leveraged public support to implement first-round reforms. The upcoming legislative elections will be crucial for gaining the mandate needed to pursue deeper structural changes, including labor market deregulation and trade liberalization.

Argentina’s long-term potential remains substantial, supported by its vast natural resources. Continued policy consistency, export growth in strategic sectors, and a gradual move toward exchange rate liberalization will be key to unlocking sustainable growth and investor confidence.

1. Executive Brief overview of Argentina's current economic and political environment

The rise of Javier Milei as President of Argentina in December 2023 initially captured international attention for his eccentricity. However, by the end of 2024, the focus of global investors had shifted to the economic achievements of his first year in office, during which he managed to steer the country away from another major economic crisis. 2024 was marked by key milestones for Argentina’s economy: an unprecedented fiscal consolidation not seen in over a decade, a significant deceleration in inflation, and a much milder recession than initially anticipated.

Argentina’s economic policies under the new administration have made remarkable strides, laying a solid foundation for economic stability and growth. The approach focuses on tackling chronic structural issues such as fiscal imbalance, inflation, and currency misalignment, which have historically undermined the nation's potential. The overarching strategy emphasizes fiscal discipline, monetary contraction, and exchange rate adjustments.

Among the standout accomplishments was the fiscal surplus, achieved through discipline that exceeded expectations in both scope and sustainability. This, in turn, contributed to reducing economic volatility. Additionally, the government successfully managed the exchange rate gap and implemented a monetary policy that anchored inflation expectations. These efforts resulted in a more predictable economic context—an invaluable asset in a historically volatile economy. Complementing this favorable balance were a relatively calm social environment, a political agenda aligned with economic objectives, and a recovery in credit activity, painting a largely positive picture.

However, Argentina’s potential for sustained growth continues to be shaped by its structural strengths and long-standing challenges. The country is endowed with significant resources, such as the second-largest lithium and shale gas reserves globally, as well as vast solar and wind energy potential. Argentina also ranks among the top producers of soybeans, corn, and beef, with further opportunities in biotechnology, tourism, and knowledge-based services. Despite these advantages, decades of poor economic policies and structural inefficiencies have hindered the full realization of this potential.

The new administration, under President Javier Milei, has initiated reforms aimed at stabilizing the economy and reducing volatility. With a history of excessive economic swings—including 24 years of GDP contraction since 1970 and an average annual growth rate of just 1%—addressing these structural challenges is paramount. Key measures include fiscal adjustment, exchange rate alignment, and monetary contraction to position the Central Bank to free the currency. While these efforts have achieved initial successes, the road ahead is fraught with challenges, including an oversized state, a heavy tax burden, and an insolvent pension system.

Looking ahead to 2025, sustaining this year's progress will require building on these reforms to unlock Argentina’s vast potential. This includes fostering exports in strategic sectors, creating quality jobs, and advancing long-term economic stability. However, this must be achieved amidst significant hurdles, such as strengthening international reserves, reducing poverty, addressing exchange rate misalignments, and navigating the uncertainty of an election year. An agreement with the IMF and the eventual removal of capital controls remain key factors on investors’ radar. However, we do not see this as likely before the legislative elections, as the government is prioritizing exchange rate stability due to its direct impact on inflation dynamics. While progress on fiscal and monetary stabilization has strengthened confidence, the timing of such an agreement will likely depend on political dynamics and the government's ability to sustain a trade and financial surplus. In the meantime, financial inflows remain critical for external stability.

At the same time, external risks add another layer of complexity to Argentina’s outlook. The global economic landscape remains volatile, with financial tightening in major economies, geopolitical tensions, and fluctuating commodity prices posing risks that could impact Argentina’s recovery. In particular, the evolution of global interest rates and capital flows will be crucial in determining Argentina’s access to external financing and its ability to gradually lift capital controls. A slowdown in global demand for key exports or higher borrowing costs could weigh on growth, making it imperative for Argentina to continue reinforcing its fiscal position, external buffers, and trade competitiveness. Sustaining a strong trade balance and attracting foreign investment will be critical in mitigating the impact of adverse global developments.

Expanding international reserves, stabilizing capital inflows, and lifting capital controls remain the most pressing challenges. However, Argentina's vast natural resources, competitive sectors, and strategic reforms provide a pathway for robust growth if policy consistency is maintained. Successfully navigating both domestic and external risks will be crucial to consolidating the country's transformation and ensuring long-term economic stability.

2. Macroeconomic Overview

i. GDP Growth: Recent trends, forecasts, and key drivers.

After a deep contraction at the end of 2023 and in the first months of 2024, Argentina’s economy has shown clear signs of recovery. By November 2024, economic activity had expanded for seven consecutive months, recovering to the level recorded in November 2023. This rebound confirms that the recession was both shorter and shallower than initially anticipated. While the economy is expected to close 2024 with an overall contraction of 2.3%, the strong carry-over effect into 2025—estimated at 3 percentage points—sets a solid floor for growth this year. However, the recovery has been highly uneven across sectors. The urban economy remains the most affected, with construction and manufacturing still operating below pre-crisis levels. The cumulative GDP contraction in urban sectors reached 4.9% y/y through November, reflecting the lagging impact of tight fiscal and monetary policies on demand-sensitive industries.

Despite the broader economic downturn, some sectors have outperformed the rest of the economy, acting as pillars of resilience and recovery. Agriculture was the main driver of economic growth, benefiting from a strong harvest after the severe drought of 2023. In 2024, the sector recorded an annual expansion of 33%, providing a crucial stabilizing factor for the broader economy. However, the sustainability of this rebound remains uncertain as recent concerns over soil moisture conditions could weigh on future yields. Meanwhile, energy and mining continued their uninterrupted expansion from 2021 to 2024, capitalizing on Argentina’s vast natural resources. The development of Vaca Muerta strengthened Argentina’s role as an energy exporter, with surplus production increasingly directed to international markets.

In contrast, urban sectors remained under pressure. The construction sector suffered from a drastic cut in public investment, while falling real wages constrained private spending, particularly in small-scale projects such as home renovations. Despite recent signs of stabilization, construction remains well below its pre-recession level. Manufacturing activity remained subdued due to weaker domestic demand, trade normalization measures that increased import competition, and lingering disruptions in input supply chains. However, the agro-industrial segment, particularly in processed crop derivatives, is expected to benefit from the agricultural recovery. Commerce and services were also severely affected by the decline in real wages and the initial drop in disposable income, but the gradual improvement in employment and consumer confidence suggests a modest recovery in 2025.

While the economy is on track to return to pre-recession levels in 2025, the long-term challenge remains the reversal of Argentina’s decade-long stagnation in productivity and GDP per capita. The success of the stabilization plan has laid the foundation for renewed growth, but its sustainability will depend on structural reforms aimed at deregulation, trade normalization, and labor market flexibility. Argentina’s economic trajectory is shifting from stabilization to expansion, but the pace and consistency of this recovery will be determined by the successful execution of these long-term adjustments.

ii. Inflation: Current rates and expectations

Inflation in Argentina has decelerated significantly, marking a turning point after years of high volatility. In 2024, inflation closed at 118% y/y, a sharp improvement from 211% y/y in 2023. The fourth quarter of 2024 saw an average monthly inflation rate of 2.6% m/m, the lowest since late 2020, with an annualized pace of 36% y/y, far below the 464% y/y rate of the same period in 2023. December inflation stood at 2.7% m/m, the lowest figure for the final month of the year since 2018, reflecting the government’s commitment to addressing structural imbalances.

This progress is largely attributed to the administration's fiscal and monetary anchors. The sharp reduction in public spending, curbing of Central Bank deficit financing, and a strict control over monetary issuance have stabilized inflation expectations. Additionally, the government’s exchange rate strategy, which maintained a 2% m/m adjustment throughout 2024, played a key role in the disinflation process, albeit at the cost of growing exchange rate misalignment.

However, inflationary pressures persist. Core inflation, which excludes regulated and seasonal prices, reached 3.2% m/m in December, reflecting wage adjustments and rising service costs, while regulated prices increased 3.4% m/m, driven by adjustments in public transport, utilities, and healthcare.

Looking ahead to 2025, inflation is expected to moderate further, with projections suggesting an annual inflation rate of 25% y/y by December. To reinforce this trend, the government has implemented policies to address inflation inertia and manage exchange rate flexibility, notably by reducing the crawling peg to 1% m/m starting in February 2025. This measure aims to stabilize goods prices and accelerate inflation convergence, supporting an expected monthly average of 1.5% m/m by mid-year, with goods prices rising 1% m/m and services 2.5% m/m.

While these projections reflect the success of fiscal and monetary reforms, risks remain. The delayed adjustment of relative prices, particularly in the exchange rate and regulated tariffs, could pose challenges in the medium term. Nevertheless, the administration’s focus on fiscal discipline, monetary stability, and gradual exchange rate flexibility has laid a strong foundation for sustained disinflation and improved economic fundamentals.

In sum, a decisive shift in fiscal, monetary, and FX policies has stabilized inflation expectations, restored public confidence, and positioned the economy on a path toward sustainable price stability.

iii. Currency Exchange Rates and International Reserves: Recent movements, central bank interventions.

Argentina’s external sector remains under strain as the country navigates the consequences of exchange rate misalignment and capital controls. Despite closing 2024 with a record trade surplus of USD 18.9 billion, this is expected to narrow in 2025, not only due to a rebound in imports following the end of the recession but also because the agricultural sector’s contribution will be lower than in 2024. At the same time, net reserve accumulation will remain a key factor to monitor, as the current account turned negative in the second half of 2024 and is expected to remain in deficit throughout 2025. As a result, the ability to build reserves will increasingly depend on financial account inflows.

One of the key challenges ahead is the impact of the ongoing drought on agricultural exports, which accounted for a significant portion of last year’s surplus. While the 2023/24 harvest led to a sharp increase in export revenues, weather conditions are now deteriorating. By the end of January 2025, 42% of soybean fields were classified as experiencing regular to drought conditions, raising concerns about future yields. Current projections suggest that soybean production could reach 49 million tons and corn 50 million tons, but a worsening drought could reduce these figures further. In an effort to stimulate early export liquidations, the government temporarily reduced export duties, a measure that could add up to USD 2 billion in additional FX inflows in the first half of 2025. However, the overall trade surplus is expected to shrink to around USD 12 billion, as higher imports—driven by currency appreciation and the end of the recession—begin to offset export gains.

Net reserve accumulation is also facing pressure from a reversal in the current account trend. While the first half of 2024 recorded a strong current account surplus of USD 8.9 billion, the second half saw a sharp deterioration, culminating in a USD 7.2 billion deficit in the last six months of the year. This shift was largely due to rising import payments, particularly in December, when the goods balance turned negative for the first time in 2024. A key driver of this deterioration was the removal of the PAIS tax, which had previously discouraged certain imports.

Beyond the trade sector, financial outflows remain a persistent challenge, particularly in terms of interest payments and foreign currency obligations. In 2024, USD 11.8 billion was paid in interest, the second-largest annual outflow since 2003, with USD 3.1 billion allocated to the IMF alone. These commitments, combined with the continued repayment of public sector foreign debt, have exacerbated the negative trend in net international reserves, despite ongoing efforts to rebuild the Central Bank’s balance sheet.

However, the financial account provided some relief in 2024, ending the year with a USD 4.3 billion surplus, largely driven by USD 2 billion in dollar-denominated loans to private companies and USD 1.4 billion in inflows from international organizations, most notably from the World Bank. This inflow partially offset the first net outflow of foreign direct investment (FDI) by non-residents since at least 2003, with USD 695 million in capital leaving the country.

Overall, the foreign exchange balance improved by USD 17.1 billion compared to 2023, primarily due to the turnaround in the financial account, which shifted from deficit to surplus with an USD 11 billion improvement, and a USD 7.7 billion increase in the trade balance. While this reversal was a positive development, maintaining this trend will be challenging in 2025, given the expected reduction in the trade surplus and the growing burden of external payments.

Looking ahead, the government faces a delicate balancing act between prioritizing inflation stabilization and gradually moving toward exchange rate liberalization. While the decision to lower the crawling peg to 1% monthly reinforces the disinflationary path, it has further deepened real exchange rate appreciation, which could undermine competitiveness and increase pressure on reserves. The official exchange rate is currently 45% lower in real terms than in December 2019, a level that historically has only been sustainable with access to significant external financing. Given the persistent capital controls and the lack of foreign credit, maintaining the current system could prove increasingly difficult.

Ultimately, the external sector remains the most fragile pillar of the economic program, with the government relying on a combination of financial inflows and trade adjustments to manage short-term volatility. Whether these measures will be enough to prevent further deterioration in reserves and maintain external stability remains a key risk for the months ahead.

iv. Public Debt and Fiscal Deficit: Levels, trends, and implications for investors

Argentina achieved a historic fiscal correction in 2024, closing the year with a primary surplus of 1.8% of GDP and a financial surplus of 0.3% of GDP—a stark contrast to the 2.7% primary deficit and 4.4% financial deficit recorded in 2023.

The correction was driven primarily by a sharp contraction in primary spending, which fell 27% y/y in real terms, far exceeding the 6% y/y decline in real revenues. The spending cuts were concentrated in key areas: public works contracted by 77% y/y in real terms, non-automatic transfers to provinces by 68% y/y, subsidies by 34% y/y, social programs by 33% y/y, pensions by 14% y/y, and public sector wages and university funding by 20% and 23% y/y, respectively.

Despite achieving a financial surplus, capitalized interest payments reached 2% of GDP, meaning that, if fully accounted for, the financial deficit would stand at 1.7% of GDP. This accounting adjustment reflects the absorption of Central Bank debt by the Treasury, a key component of the government's broader strategy to clean up the financial system.

The fiscal adjustment was not limited to the national government but also extended to provincial administrations, which were forced to cut spending due to reduced federal transfers. This led to a rare consolidated fiscal surplus, a phenomenon that has only occurred six times in Argentina’s last 60 years.

Maintaining fiscal equilibrium in 2025 seems to be largely priced in, although it still presents a challenge as revenue pressures mount with the elimination of the PAIS tax, the expiration of the tax amnesty program, and the end of the tax moratorium, all of which will reduce overall tax collection. At the same time, spending pressures are set to rise, particularly due to pension and child benefit adjustments linked to the mobility formula. To compensate for these revenue losses, economic growth is expected to contribute 0.6 percentage points in additional tax revenue, while interest payments on debt are projected to decline from 1.5% to 1.3% of GDP, providing some relief to public finances. Additionally, continued subsidy reductions and adjustments in fuel taxes could generate another 0.7% of GDP in savings.

The government has demonstrated a strong commitment to maintaining fiscal discipline, with financial balance remaining a non-negotiable priority. Even recent measures, such as the temporary reduction in export duties, which will impact revenues by approximately 0.1%-0.15% of GDP, are expected to be offset by further spending cuts, avoiding any significant fiscal risks.

At the same time, in December 2024, the Treasury debt reached USD 466.7 billion, equivalent to 83% of GDP, marking an increase of USD 96 billion over the year and USD 41 billion compared to November 2024. Of this total, 45% is denominated in local currency, with 16% non-indexed and 29% linked to inflation (CER), while the remaining 55% is in foreign currency, primarily in U.S. dollars (45%) and IMF Special Drawing Rights (SDRs), which account for 8.7% of total debt (USD 40 billion). In December alone, debt rose by USD 2.4 billion due to new issuances and valuation adjustments. Over the course of 2024, net financing from international organizations was negative, with the IMF recording a net outflow of USD 3 billion. The appreciation of the peso played a key role in driving up the debt-to-GDP ratio, as dollar-denominated obligations increased in real terms. While the fiscal anchor has strengthened confidence in Argentina’s economic outlook, the rise in public debt underscores the importance of sustaining fiscal discipline and carefully managing financing strategies in 2025.

3. Political Landscape and Risks

i. Overview of the current government and its economic policies

The current administration has reinforced its political standing in recent months, supported by a resumption of real GDP growth and a recovery in economic activity. Poverty rates have fallen sharply, dropping from 54.8% in 1Q24 to 38.5% in 3Q24, as real incomes have recovered alongside improved employment levels. This economic progress has bolstered public support for the government’s policies, further reflected in the Government Confidence Index (GCI), which stood at 52% in January 2025. Regional disparities persist, with higher confidence levels in the interior of the country (57%) compared to Greater Buenos Aires (45%), highlighting both socio-economic divides and stronger opposition presence in urban areas.

At the outset, the administration faced significant institutional limitations, holding only a minority presence in Congress with 38 deputies and 8 senators—approximately 15% and 11% of total seats, respectively. This constrained its ability to advance structural reforms through legislative channels, requiring greater reliance on executive measures, emergency decrees, and negotiated agreements to push forward its economic agenda. However, the government has managed to capitalize on its broad public support, securing early wins in deregulation and fiscal consolidation while avoiding major political gridlock. By strategically prioritizing reforms that require less congressional approval, it has gained initial momentum, though larger structural changes remain dependent on an improved legislative standing.

Looking ahead, the 2025 legislative elections will be crucial for solidifying the government’s position in Congress, as its sustained public approval suggests a strong electoral performance. A larger congressional presence would significantly enhance its ability to advance deeper structural reforms, particularly in pension restructuring, tax system simplification, and further labor market flexibility. However, some political challenges remain. Internal tensions within the ruling coalition and ongoing friction with its ally, the PRO, pose risks to stability. Additionally, polarization with Kirchnerism, particularly in Buenos Aires Province, could further entrench political divisions. These factors underscore the need to closely monitor the political environment, especially in the lead-up to the elections.

The government’s prioritization of inflation reduction remains a cornerstone of its strategy to maintain public support. While inflationary pressures have eased significantly, with inflation dropping to 24% y/y in 2025, this achievement has come at the cost of delaying other necessary economic adjustments, such as the liberalization of exchange controls. The administration has also adjusted its exchange rate policy, reducing the crawling peg to 1% monthly, which has further stabilized inflation expectations but at the expense of greater peso appreciation, potentially leading to future volatility.

Overall, while the political environment is broadly favorable for the administration, sustained public support and careful coalition management will be key to navigating both legislative elections and ongoing economic challenges.

ii. Structural economic reforms ongoing

Argentina’s economic reform agenda has expanded beyond fiscal consolidation, with the government actively pursuing structural changes aimed at enhancing competitiveness and fostering long-term growth. In addition to substantial spending cuts and monetary tightening, recent initiatives have focused on deregulation, trade liberalization, labor market reforms and improving public sector efficiency.

At the core of these reforms is a significant shift in trade policy. The government has implemented measures to reduce tariff barriers and simplify import processes, aiming to enhance competitiveness in key sectors like agriculture, energy, and manufacturing. The reduction of the PAIS tax on imports has played a crucial role in stabilizing domestic prices and lowering production costs. Following a 10-percentage-point cut in the tax in September, the prices of imported food and beverages decreased in real terms by an average of 2.4%, demonstrating the immediate impact of trade liberalization on consumer prices. Additionally, efforts to streamline bureaucratic trade restrictions have begun, easing access to essential inputs for businesses.

Another key pillar of the reform agenda is the restructuring of the labor market. Argentina has not created private-sector jobs in over a decade, while public-sector employment has continued to expand. The government has reversed this trend by reducing the state payroll, cutting 36,000 public-sector jobs between December 2023 and November 2024—representing a 7.2% decrease in total public employment. These cuts have generated fiscal savings exceeding USD 4 billion. Simultaneously, labor market reforms embedded in the ‘Ley Bases’ legislation seek to incentivize private-sector hiring by extending trial periods, reducing severance penalties, and lowering the cost of formal employment.

Additionally, the administration is advancing an ambitious energy agenda. Argentina's energy sector remains a key driver of structural improvements in the external accounts, with Vaca Muerta's growing output supporting increasing crude oil and gas exports. The government is prioritizing infrastructure investment in energy transport and refining capacity to boost Argentina’s trade surplus in the medium term.

Looking ahead, the 2025 midterm elections will be critical in determining whether the government can gain a stronger congressional foothold to advance deeper structural changes, particularly in areas such as tax reform, pension restructuring, and further deregulation.

While significant challenges remain—particularly in sustaining macroeconomic stabilization, maintaining social and political cohesion, and securing external financing—Argentina’s reform trajectory signals a strategic shift towards a more competitive and market-driven economy. The success of this agenda will depend on the government's ability to sustain momentum, secure necessary political backing, and effectively manage short-term trade-offs between disinflation and economic recovery.

4. Scenario Analysis and Forecast

Based on the December 2024 market expectations survey (Central Bank's "Relevamiento de Expectativas de Mercado"), projections for 2025 indicate an improving economic outlook with a rebound in growth, moderating inflation, and a stronger fiscal position.

After an estimated contraction of 2.6% in real GDP during 2024, the economy is projected to grow by 4.5% in 2025, supported by recovery in key sectors and a return to pre-pandemic growth trends.

Following an annual inflation rate of 118% in 2024, inflation is forecast to decelerate significantly in 2025, with projections suggesting an annual rate of 25.9%. The core inflation component is expected to align closely with the general inflation trend, supporting expectations of macroeconomic stabilization.

The exchange rate, projected to average ARS 1,042/USD in January 2025, is expected to reach ARS 1,205/USD by December 2025, reflecting a year-on-year nominal depreciation of 18.1%, though at a slower pace compared to recent years.

The primary fiscal surplus is expected to improve substantially, reaching ARS 11.2 trillion in 2025, reflecting fiscal consolidation efforts. No primary deficit is anticipated for 2025 or 2026.

Trade expectations remain strong, with exports projected to reach USD 82.8 billion and imports USD 67.4 billion in 2025, resulting in a trade balance of USD 15.4 billion, slightly below the USD 18.9 billion recorded in 2024. This figure could be even lower, as crop yield estimates were not updated at the time of the Central Bank's survey.

The main risks highlighted include external factors such as potential shifts in exchange rate policies or global financial conditions, which could introduce volatility into inflation and economic recovery trajectories. Nonetheless, the overall outlook for 2025 points to stabilization and gradual improvement.

5. Alert and Opportunity Dashboard

.avif)