Following the recent FX correction and interest rate adjustment, the market is beginning to offer more favorable conditions for the carry trade, albeit in an environment that still calls for caution. With rates now at a higher level, opportunities are emerging in ARS-denominated instruments offering elevated yields. In this context, dual bonds have gained appeal by capturing high nominal rates without forgoing FX protection. We maintain our positioning in CER-linked bonds given projected inflation above the levels implied by the market, and we retain a constructive view on dollar-linked instruments, complemented by locally issued corporate bonds that combine liquidity with attractive spreads.

In our recent reports, we had suggested reducing exposure to ARS carry trades and starting to dollarize part of the portfolio. This strategy proved accurate: in July, the official exchange rate rose 13.2%, while financial dollar rates followed suit, resulting in negative returns for carry trade strategies. Despite that performance, we now see attractive entry points in certain peso-denominated instruments.

Following the monetary rebalancing that triggered significant volatility in interest rates, peso yields appear to be stabilizing—albeit at a meaningfully higher level. The fixed-rate curve remains clearly inverted, with yields ranging from 41% NAR in the short end to 32% NAR in the long end. These levels appear to be consolidating as a new equilibrium point, in a context of FX pressures and a particularly demanding peso maturity profile in the coming months—ARS 36.5 trillion in August and ARS 20.1 trillion in September—remaining challenging into year-end. While the Treasury holds ARS 14.2 trillion on its BCRA account, it is expected to seek to sustain a high rollover rate, which would require continuing to validate high rates in order to prevent excess liquidity from depressing yields and spilling over into the FX market, potentially jeopardizing the disinflation process. Against this backdrop, while we continue to recommend maintaining a significant portion of the portfolio in hard currency, we identify opportunities to re-enter peso instruments at current FX and interest rate levels.

Fixed-Rate Curve

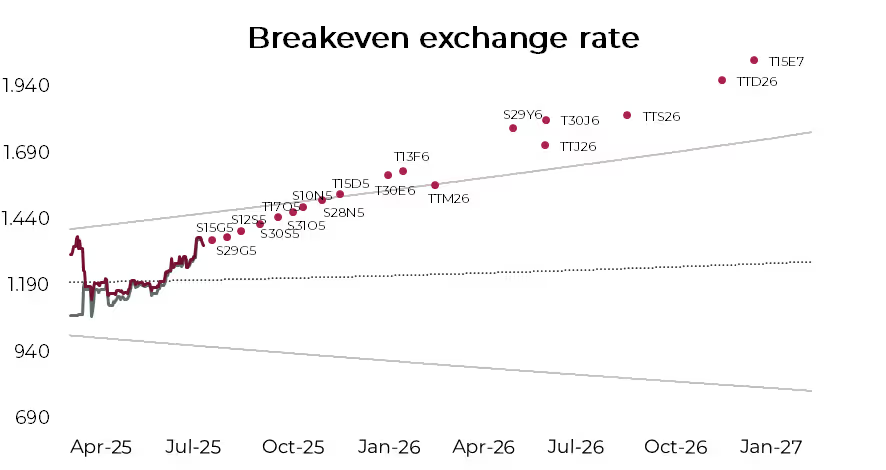

As shown in the chart, starting from the Boncap T15D5, the breakeven FX rate begins to exceed the upper bound of the FX band. This implies that, under the current FX regime, an investor acquiring this bond today and holding it to maturity on December 15 could achieve a direct USD return of at least 0.5% (1.4% NAR). Beyond that point, potential returns become increasingly attractive. For longer maturities, such as the T15E7—maturing in January 2027—the direct USD return rises to 17.4% (11.8% NAR), assuming the band regime remains in place and its mechanics unchanged. These returns could be even higher if the FX rate remains below the calculated breakeven level.

Dual Bonds

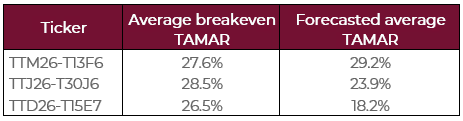

On the other hand, dual bonds continue to present themselves as an attractive alternative, especially given the persistence of higher nominal rates in the short term, which could be captured through these instruments. Recall that duals pay the higher rate between the compoundable fixed rate and the average TAMAR (variable) rate from the issuance date to the maturity date. Observing the evolution of TAMAR, it stands at 43.8% nominal annual rate (TNA), almost 10 percentage points above the levels prior to the end of LEFIs. In this context, if we project the rate these instruments would accrue by maturity under our base scenario—which contemplates a gradual reduction in nominal rates toward maturity, although remaining elevated in real terms—we estimate that both the TTM26 and TTJ26 duals would end up paying the variable rate, implying a direct yield of 23.4% and 31.3%, respectively. In contrast, the TTS26 and TTD26 bonds would pay their fixed-rate version. However, the average breakeven TAMAR rate between today and the maturity date—i.e., the rate that would equal the yield of the fixed-rate alternative—stands in a range of 26.5% to 28.5% TNA. These levels are higher than our wholesale rate projections for the entire period in the cases of the TTJ26, TTS26, and TTD26 bonds, indicating that these instruments would likely end up yielding less than their fixed-rate counterparts. The only exception would be the TTM26, for which we project an average TAMAR rate above its breakeven, implying a relatively favorable yield compared to the fixed-rate option.

CER Curve

Taking into account our base scenario, which contemplates inflation somewhat higher than initially expected—due to the faster pace of devaluation—we maintain our positioning in CER bonds. As we mentioned in Recalibrating the Peso Curve, these instruments currently exhibit real rates of around 18% per year. Thus, the average implied inflation stands at 2% m/m until October 2025 and at 1.8% m/m from November to January 2026, below our estimates, which foresee a slight acceleration in inflation after the elections. In particular, we highlight the TZXM6 (CER +19.2%) and the TZXD6 (CER +16.1%), not only because they show very attractive real rates, but also because they would allow capturing the potential acceleration in prices as a result of an increase in the pace of devaluation.

Dollar-Linked Curve

For investors seeking to mitigate exchange rate risk, we maintain a favorable view on dollar-linked debt, which continues to lead year-to-date performance with a 29.6% gain. In particular, we still see value in the TZVD5, which trades at a devaluation rate +9.3%, incorporating a direct implied devaluation of 9%, below the 14% we estimate in our base scenario. Moreover, it far exceeds the return of synthetic dollar-linked instruments with similar maturities, built from the purchase of a Lecap and a futures contract with matched maturities. Nonetheless, we also find it interesting to complement the strategy with locally governed corporate bonds, which currently combine higher liquidity with attractive spreads, with notable options including Tecpetrol 2026 TTC7O (5.7% YTM) or YPF 2027 YM35O (6.8% YTM).