Argentina’s financial landscape reached aninflection point in recent days. Prior to the external support announcements,uncertainty following the Buenos Aires Province elections had effectively endedthe “electoral trade,” delivering heavy losses to local assets. Between theMonday after the vote and Friday, September 19, sovereign bonds in dollarsdropped on average 22%, driving country risk to 1,456 bps, the highest sinceSeptember 2024. The Merval plunged 24.6% in dollar terms, while the official exchangerate rose 8% and tested the upper bound of the FX band. Mounting pressureforced the BCRA to sell USD 1.11 billion to defend the band ceiling, as pesoyields spiked—October Lecap jumped from 70% effective annual rate (EAR) to 87%EAR. The market began to price a tighter external constraint, combined with thegovernment’s diminished ability to advance reforms in Congress, prompting asharp dollarization of portfolios.

The market’s tone shifted abruptly afterpolitical and economic signals from Washington. U.S. Treasury Secretary ScottBessent stressed Argentina’s role as a strategic ally and highlighted progresson fiscal consolidation and price liberalization, announcing a support packageincluding:

• Willingness to buy sovereign bonds in dollarsin primary or secondary markets.

• Negotiation of a USD 20 billion swap with theBCRA.

• Potential credit line via the ESF.

• Coordination to normalize tax incentives forthe export sector and facilitate private investment, subject to the Octoberelection outcome.

These measures were reinforced by commitmentsfrom multilaterals: the World Bank would front-load disbursements of USD 4billion, while the IDB would expand and accelerate operations in the country.In parallel, the government temporarily suspended agricultural export duties tospeed up FX inflows.

The market reaction was immediate and positive.Between Monday and Wednesday, sovereign bonds in dollars rebounded 29% and theMerval in dollars surged 23%. In pesos, the October Lecap EAR dropped from 87%to 54%, while exchange rates fell—down 8% for financial rates and 11% for theofficial—narrowing the gap from 5.5% to 2.6%.

This sequence redefined pre-election risk.Before the announcements, FX pressure was intensifying as market accessappeared increasingly remote and the economic program looked fragile. Concernsover debt sustainability were mounting, with the Central Bank forced to selldollars at the band ceiling instead of accumulating reserves. With U.S.support, part of the financing gap would now be covered through the financialaccount, easing immediate tensions and allowing the government to face theelections with greater calm. Political risk remains, but the market is nolonger as exposed: external backing strengthens near-term conditions and lowersthe likelihood of disruptive episodes before the vote.

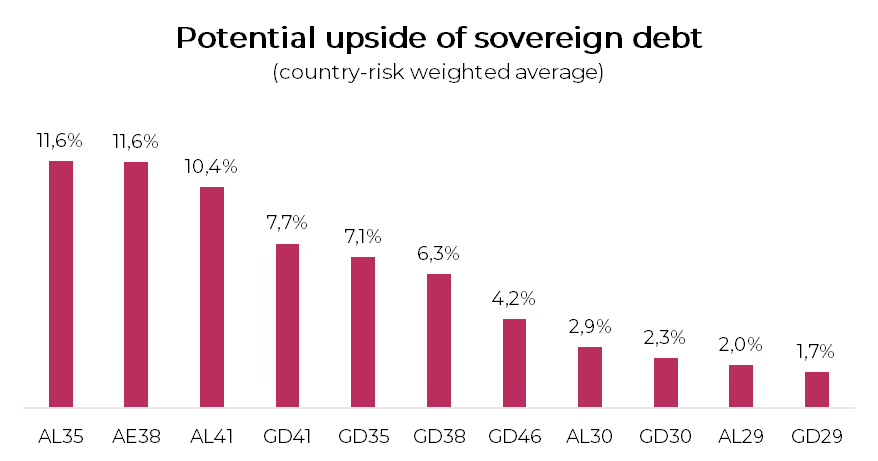

Against this backdrop, sovereign bonds stillshow upside into October. Greater predictability around payments is improvingsentiment and creating room for further spread compression. Under scenarioweighting, we assign high probability to country risk converging toward the675-bps range—levels similar to those seen after the Buenos Aires Cityelections—thus enabling additional yield compression. Unlike that episode,today’s political front is weaker, with the ruling coalition constrained by thePBA setback and tensions in Congress. Economically, however, the backdrop looksmore consistent: despite weaker activity, a higher real exchange rate hasimproved external balances, while international backing provides an additionalfunding source that strengthens the framework.

Dollar-denominated strategies

Within this new setup, Bonar bonds—whichunderperformed ARGENT bonds during the correction—offer greater recoverypotential. At the same time, Bopreal instruments also stand out, with room foradditional spread tightening. Among sovereign debt, we highlight Bonar AL35(14.1% YTM) and AL41 (13.7% YTM), which combine higher liquidity with superiorreturn potential should country risk compress toward 675 bps, implyingpotential gains of 11.6% and 10.4%, respectively. We also emphasize BoprealSeries 4 (17% YTM), which, despite low liquidity, offers higher yields thanAL29 and AL30, with estimated upside of 10.8%, in addition to the tax benefitof applying it toward payment of fiscal obligations.

ARS-denominated strategies

Even with the recent improvement in marketexpectations, FX dynamics remain vulnerable. Looking ahead to the post-electionperiod, the Central Bank will need to rebuild reserves through FX purchases, aprocess that will add pressure on the exchange rate and make it difficult tosustain a band-based regime over the medium term.

In the short term, conditions look morefavorable. Lower FX pressure allowed the BCRA to intervene in the repo marketon BYMA, cutting the rate from 35% to 25% NAR, supported by improvedexpectations and higher agricultural FX inflows expected in the coming days.This rate cut is boosting demand for Treasury instruments while easing strainson activity, at the same time reducing the appeal of local-currency carrytrade.

Within ARS-denominated strategies, we favorpositioning in dollar-linked instruments, particularly the TZVD5 (3.5% EAR),which embeds an implied devaluation of 8.4% (equivalent to 3% m/m) towardDecember of this year. In addition, hedging through January dollar futurescontracts emerges as an attractive alternative: market pricing reflects anexchange rate at the band ceiling with a relatively low hedging cost (38.9%NAR) compared to the yield of a Lecap of the same maturity (45.9% NAR),enabling synthetic dollar-linked strategies.

For the rest of the peso universe, we prefer tostay at the short end of the curve and favor CER-linked bonds over fixed-rateinstruments. In particular, we highlight the TZXD5 (23.5% YTM), which impliesaverage monthly inflation of 1.6% between September and October, a level thatlooks relatively low compared with our projections.