On September 7th, legislative elections were held in the Province of Buenos Aires to renew 46 seats in the Chamber of Deputies and 23 in the Senate, in addition to municipal and school council positions. Peronism, under the Fuerza Patria banner, secured a decisive victory with roughly 47% of the vote, outpacing La Libertad Avanza (LLA) by more than 13 percentage points, as the latter obtained between 33% and 34%. The defeat of the ruling coalition was broad across most electoral districts—particularly the First, Third, Second, Fourth, Seventh, and Eighth—while LLA only prevailed in the Fifth and Sixth. The result represents a major setback for the Milei administration and consolidates Governor Axel Kicillof as the leading opposition figure heading into 2027, while adding uncertainty over the outcome of the upcoming national legislative elections in October.

Ahead of the Buenos Aires provincial election, polls gave LLA a narrow lead, yet the market had already priced in a setback for the government, albeit without gauging its magnitude. By the prior Friday’s close, sovereign dollar bonds were yielding around 15%, with country risk near 900 bps and the Merval at USD 1,445. Once the results were in, dollar-denominated debt plunged 8.7% in a single session on Monday, pushing average yields to 17% and country risk to 1,100 bps, while the Merval collapsed 17% in dollar terms to USD 1,196. On Tuesday and Wednesday, there was a partial rebound—with bonds recovering 3.7% and the equity index rising 6.5% to USD 1,274—but the cumulative correction underscored that, while markets had anticipated an adverse outcome, they had not fully internalized the extent of the ruling party’s defeat.

Against this backdrop, the run-up to the October national legislative elections appears increasingly challenging, with a weakened government and a market already pricing in a higher risk premium, reflecting concerns over governance and the viability of the economic program. In this environment, the electoral trade loses traction and attention shifts toward medium-term dynamics, where the Buenos Aires result establishes a high floor for the Peronist Party and poses a more adverse scenario for La Libertad Avanza to secure a favorable outcome.

The central question is which market dynamic could prevail under this scenario. A lackluster result for the ruling coalition would reinforce market distrust, with country risk remaining far from easing from current levels. In the absence of capital account inflows, external balance would need to be achieved through a higher real exchange rate and greater reserve accumulation by the Central Bank. If sustained, this would imply that the official exchange rate surpasses the upper bound of the band, with the attendant risk of accelerating inflation.

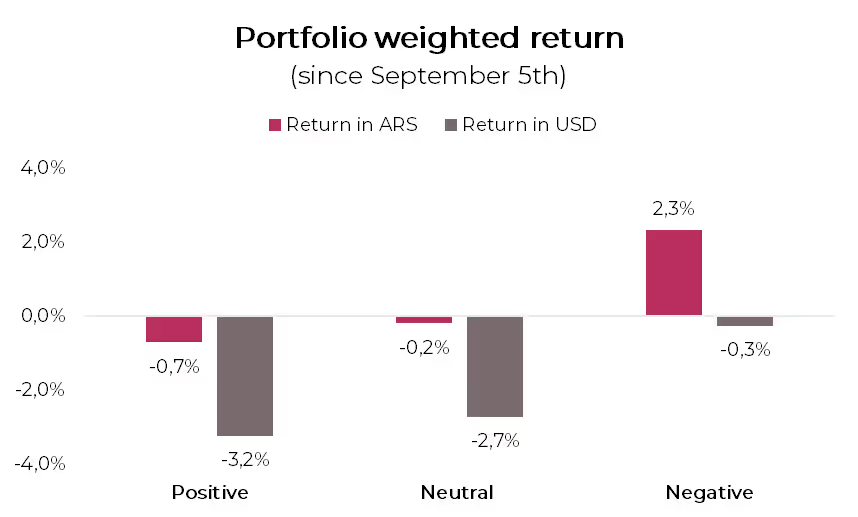

In Countdown to the Electoral Trade we laid out this analytical framework and, on that basis, constructed different portfolios to navigate each scenario. As the chart illustrates, the portfolio designed for an adverse scenario proved the most resilient (-0.3% in USD), as it incorporated a significant allocation to hard-dollar instruments —including cash in USD— and diversification into corporate bonds that provided additional yield. Meanwhile, the portfolio aligned with a favorable scenario —with greater exposure to peso-denominated instruments and sovereign bonds— lagged behind, with an accumulated 3.2% decline in USD, affected by the rebound in the exchange rate and the poor performance of hard-currency sovereign bonds.

That said, and given the challenging outlook ahead, we prioritize a defensive positioning to navigate the electoral period with lower volatility, maintaining a higher allocation to dollar-denominated instruments, including corporate bonds to reduce sovereign risk exposure and strengthen hedging against potential currency pressures. We also maintain some allocation to inflation-linked bonds (CER), which currently offer real yields around 20% and provide protection against a potential acceleration in inflation, as well as to dual bonds, since a higher exchange rate together with elevated inflation could set a higher floor for rates, supporting their performance relative to fixed-rate alternatives.

Recommendation: 45% in USD cash, 40% in corporate bonds —Telecom 2026 TLC1O (6.7% YTM), Tecpetrol 2026 TTC7O (5.8% YTM)—, 10% in CER bonds —TZX26 (CER +20.9%)—, and 5% in Duals —TTM26 (TAMAR +10.3%)—.