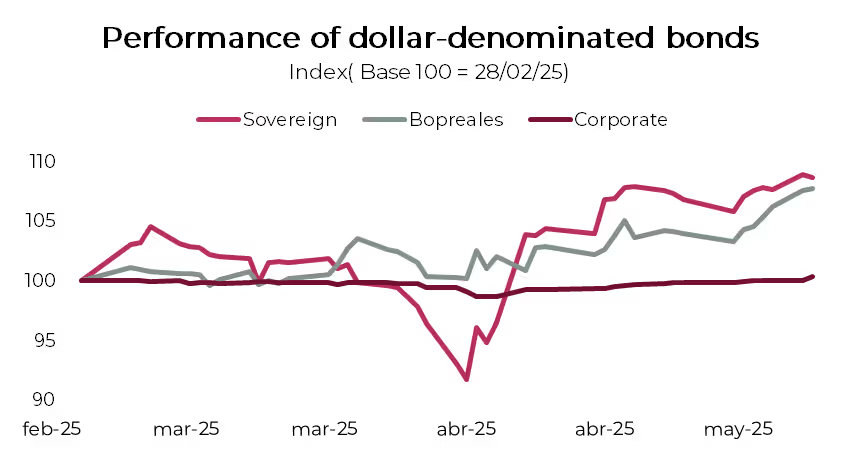

One month after the partial lifting of FX controls, it is timely to assess the recent performance of dollar instruments and their outlook going forward. In From Uncertainty to Relief, we highlighted that an agreement with the IMF would likely be a catalyst for resuming the downward trend in country risk observed throughout 2024. With the agreement now in place and the first disbursement of USD 12.300 M completed, dollar-denominated sovereign bonds have rallied 12.7% to date, bringing country risk down from 896 bps to 678 bps. The improved environment also had a positive impact on the rest of the curve, albeit more moderately as usual: Bopreal rose 5.5%, while corporate bonds advanced 1.2%.

However, challenges remain for country risk to continue declining and break below the 600 bps threshold. First, the current FX regime raises questions about the pace of reserve accumulation, as the government is prioritizing disinflation by steering the exchange rate toward the lower bound of the band, rather than intervening in the FX market through dollar purchases. Second, the upcoming October midterm elections introduce political uncertainty regarding the level of congressional representation the ruling coalition will secure. In this regard, the progress of the disinflation process will be key for the government to consolidate social support and head into the elections in a strong position. All signs suggest that the administration is currently prioritizing this objective over reserve accumulation: the BCRA’s absence from the FX market and the high trading volume in the futures market—potentially signaling indirect intervention by the central bank—are consistent with this strategy.

On another front, during the first days of July, the Treasury faces capital and interest payments on Bonares and ARGENT bonds totaling USD 4.350 M, while it currently holds USD 2.748 M on deposit at the BCRA. This means it still needs to purchase USD 1.600 M to meet those obligations. Given this dynamic and the challenges that persist, hard-dollar sovereign bonds may begin to lose upward momentum in the absence of short-term catalysts for further compression in country risk.

In this context, for more conservative investors, we believe it is reasonable to consider some tactical profit-taking on the long end of Bonares and ARGENT bonds and rotate into the BOPREAL 1-B. This instrument currently yields 10.6% (YTM), and the annual return from buying the bond today and holding the coupons without reinvestment (current yield) is 5.1%. In addition, BOPREALs have proven to be less volatile in periods of heightened uncertainty. That said, we remain constructive on the long-term potential of the Global 2035s (10.9% YTM), given their capacity to capture greater upside in the event of a decline in country risk, and their current yield of 6%, well above the 0.9% offered by the 2030 Bonares and ARGENT bonds.

Corporate Bonds

For more conservative investment portfolios, we suggest maintaining some exposure to corporate bonds. These instruments tend to exhibit lower sensitivity to local political and economic risk, while offering yields in the 6%–7% range (YTM). On the short end, we favor locally governed notes, where we see more attractive opportunities: YMCVO, with a 7% yield to maturity and a 6.25% nominal annual coupon, and YMCQO, with a 6.2% yield to maturity and a 5% nominal annual coupon. For longer-duration positions, we prefer foreign law notes, with standouts including TLCMO (8% YTM, 9.5% nominal annual coupon) and YMCXO (8% YTM, 8.75% nominal annual coupon).

ARS-Denominated Strategies

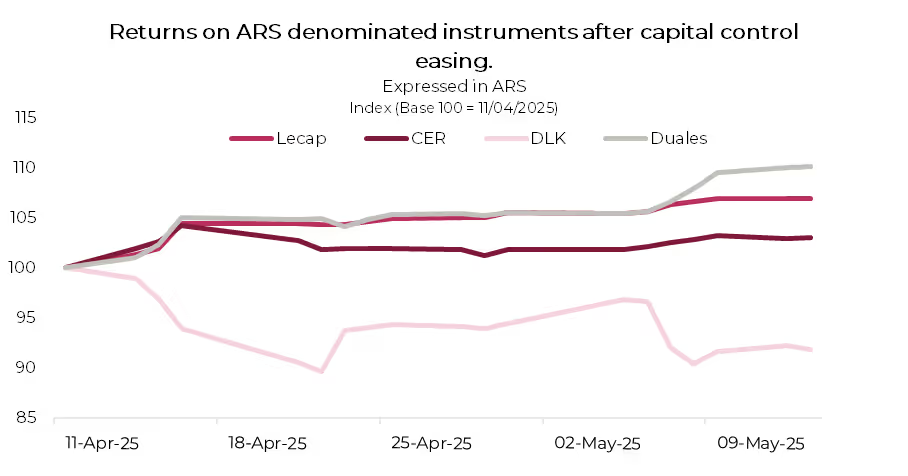

For ARS-denominated portfolios, we reaffirm our strategy of remaining positioned in the August Lecap on the fixed-rate curve, dollar-linked bonds maturing in December 2025, and CER-linked bonds maturing in March 2026. Following the government's announcement of FX regime flexibility, yields compressed sharply across both Lecaps and duals, while CER and dollar-linked bonds underperformed. With April's national inflation at 2.8% m/m, the ongoing disinflation path should support further yield compression along the Lecap curve. Meanwhile, both CER and post-election dollar-linked bonds continue to offer attractive and positive real returns.

We highlight the S15G5 (maturity 08/15/2025), offering returns of of 31.6% NAR, above the May Lecap (30.2% NAR) and June Lecap (31.1% NAR), with good liquidity. In a scenario of faster-than-expected disinflation, this intermediate segment would benefit from further yield compression. On the other hand, if the exchange rate approaches the lower band limit and the market demands higher rates to cover currency risk, the negative impact would likely be more contained in the short-to-intermediate segment compared to longer-dated Lecap or Boncap bonds.

We maintain our preference within the CER curve for TZXM6 (maturity: 03/31/2026), which yields CER +9.1%. While inflation may continue to decelerate in the short term, exchange rate pressures could resurface toward year-end due to the upcoming legislative elections, potentially passing through to consumer prices. In that scenario, this bond would capture inflation through January 2026, in addition to an attractive real rate.

Following the same logic as with the CER curve, dollar-linked bonds continue to offer elevated rates. Specifically, TZVD5 (maturity: 12/15/2025) yields devaluation +9.7%, comparable to a Bopreal Series 1-C, but with a shorter duration.

After last week’s sharp decline in dollar futures, interest in synthetic dollar-linked structures re-emerged—namely, buying a futures contract and a Lecap with matching maturity to lock in a dollar-denominated rate. However, following the rebound in futures—now pricing in an annualized rate of 25%—the returns offered by synthetic DLKs are currently lower than those of the actual dollar-linked bonds or even hard-dollar sovereigns.

Conversely, fixed-rate synthetics— which involve selling a futures contract and buying a dollar-linked bond to lock in a peso-denominated rate — are offering yields higher than Lecaps. For example, purchasing TZV25 (16.18% NAR) and selling the June futures contract (25% nominal annual rate) results in a monthly effective rate (EMR) of 3.47%, nearly 100 basis points above the Lecap S30J5’s 2.57% EMR. Although this strategy is complex, requiring margin for the futures position and daily settlement, the implied annualized rate (41.6% NAR) significantly outperforms other market alternatives.

Recommendation: For ARS-denominated investments, we suggest the following portfolio allocation: 20% S15G5 (2.54% EMR) + 20% S29G5 (2.52% EMR) + 10% TZXD5 (CER +7.9%) + 20% TZXM6 (CER +9.7%) + 15% TZVD5 (Devaluation +9.7%) + 15% TTM26 (2.1% EMR).