Argentina Economic Report

Executive Summary

The Argentine economy has experienced significant volatility in recent decades, but with the necessary structural reforms, the potential is enormous. Despite being the second-largest holder of lithium and shale gas reserves, and a major agricultural producer, decades of poor economic management have hindered sustainable growth.

The new Administration is focused on stabilizing the economy through a three-pillar reform program. President Milei’s Government is implementing fiscal adjustment, exchange rate correction, and monetary tightening. These efforts aim to address Argentina’s deep-rooted structural issues, such as an oversized public sector, an unsustainable pension system, and fiscal imbalances that have historically driven inflation.

The fiscal plan is decisive. The primary deficit, which stood at 3.3% of GDP in 2023, is expected to shift to a primary surplus of 1.5% of GDP in 2024, with similar expectations for 2025.

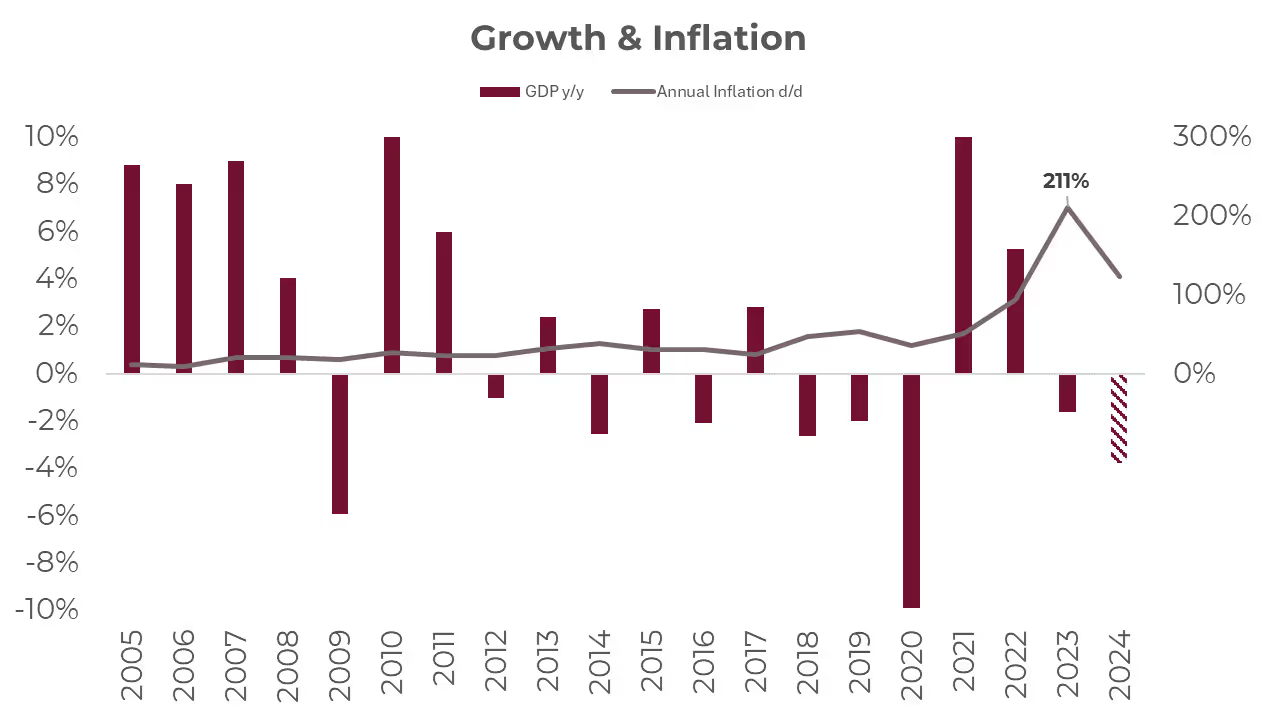

The new economic program has successfully reduced extremely high inflation, though the road ahead will be challenging. Inflation, which stood at 211% year-over-year in December 2023, is expected to peak at 120% by the end of 2024 and to moderate to 38.4% by the end of 2025. This remains as the Government’s most important asset in maintaining public support.

The downside of the plan is the economic recession in 2024, although it is expected to be overcome in 2025. The economy is projected to shrink by 3.8% in 2024 due to fiscal adjustments, but a recovery of 3.5% is anticipated in 2025 as real incomes begin to stabilize and key sectors improve.

The exchange rate regime and capital controls remain the central risk to Argentina’s recovery. The Government’s ability to manage a potential exchange rate liberalization or maintain capital controls without triggering further inflation will be critical in determining the success of its economic plan.

The reform path will not be linear, and the 2025 legislative elections will be pivotal. The limited representation of the Administration in Congress poses challenges to advancing its reform agenda. A strong mandate in the 2025 elections will be crucial. While public confidence remains high, continued support will depend on the Government’s ability to manage inflation and ensure social stability while addressing Argentina’s fiscal and monetary imbalances.

1. Overview: Argentina's current economic and political environment

Argentina has the second-largest lithium and shale gas reserves in the world, and the fourth-largest shale oil reserves. It also boasts immense potential in solar and wind energy. Additionally, it is the third-largest producer of soybeans and ranks among the top five producers of corn. There is also significant room for growth in sectors such as beef production, other agricultural products, and biotechnology. Argentina has great potential to further boost tourism and knowledge-based services, just to mention some examples.

However, decades of poor economic policies have prevented this potential from being fully realized. The country has everything it needs to grow again and embark on a path of significant transformation. To achieve this, it must first reduce inflation and stabilize the economy. Additionally, it’s crucial to remove regulatory barriers and implement reforms to boost productivity. Several strategic sectors, with a more stable macroeconomic environment, could exponentially increase exports and create quality jobs—something that hasn’t happened in 12 years.

This potential could not be developed due to the excessive volatility of the Argentine economy. In the last 80 years, Argentina only managed to grow for five consecutive years three times, and only in 13 of those years annual inflation was below 5.0%. Since 1970, GDP has contracted in 23 of those years, with an average yearly growth of 1.0%, half that of neighboring countries such as Uruguay or Chile. This growth volatility is due to recurring fiscal crises (only six years with a financial surplus in the last 60 years) and balance of payments crises, which always end in disorderly adjustments, leading to inflationary and/or debt crises.

On December 10, 2023, Javier Milei took office as President of Argentina with the mandate to change this history amidst a backdrop of deep instability. The country was facing rapidly accelerating inflation, the threat of hyperinflation, a widening fiscal deficit driven by pre-election spending, economic recession, an overvalued currency propped up by exchange controls, and rising poverty levels. In response, the new Administration swiftly rolled out an economic plan aimed at correcting the structural imbalances of the country, particularly in the areas of fiscal policy, exchange rates, and monetary management. The strategy was built on three key pillars: fiscal adjustment, the alignment of relative prices (including the exchange rate), and monetary contraction, intended to place the Central Bank in such a position to free up the currency.

Argentina’s structural issues—such as an oversized state, a heavy tax burden, an insolvent pension system, and the inequitable distribution of resources between provinces—are being addressed through ongoing reforms. Although progress has been uneven and challenges persist, particularly because of the few seats held by Milei’s party in Congress, the Government remains committed to a path rooted in basic economic principles. These include opening the economy to boost exports, recognizing that 'a bigger Government' does not necessarily mean 'a better Government', and acknowledging that printing money fuels inflation.

2. Macroeconomic Overview

- GDP Growth: Recent trends, forecasts, and key drivers.

The structural imbalances in Argentina's economy have led to a persistent decline in productivity and, consequently, a drop in GDP per capita. Argentina’s GDP has remained stagnant since 2011, with seven of the last 12 years showing a contraction in output, resulting in a GDP per capita decline of 1.0% annually.

In 2024, the economic plan aimed at addressing these structural imbalances had a significant initial impact on GDP, revealing an economic reality much harsher than what the 1.6% annual contraction in 2023 had suggested. The 2023 decline wasn’t larger because it was artificially supported by unsustainable measures, such as monetary expansion, fiscal stimulus, and an overvalued exchange rate. These factors boosted consumption as people sought to hedge against future price hikes and exchange rate fluctuations.

The fiscal adjustments had a particularly negative effect on the urban economy, with sectors such as construction, commerce, and industry expected to see declines. In construction, the reduction in public investment directly impacted a large portion of the sector, while falling real wages constrained private investment, especially in smaller projects such as repairs and home improvements.

Commerce is projected to shrink by nearly 13% in 2024 compared to the previous year. The key driver is the decline in real wages, expected to drop by 13%, particularly due to the low baseline set by the December-January period.

In the manufacturing sector, the contraction will be driven by lower real incomes, restrictions on the imports of inputs due to the efforts made to normalize payment chains after the debt buildup in 2023, and the introduction of new import sources—particularly for food and other consumer goods. However, the recovery of the agricultural harvest will have a positive impact on the agro-industrial sector, including the production of crop derivatives such as oils and flour. Overall, the industry is expected to shrink by 11% in 2024.

However, 3 out of the 15 sectors of the Argentine economy will grow in 2024, practically regardless of what happens with the other variables: agriculture, energy and mining.

The 2023/2024 harvest for Argentina’s three main crops—corn, wheat, and soybeans—is projected to generate $31.7 billion, excluding any industrial processing added-value. This would mark the fourth highest value in the last 12 years and a 24% increase compared to the 2022/2023 season, which was seriously impacted by drought. The agricultural sector, which accounts for 8.0% of the economy, is expected to grow by 33% year-over-year, driven almost entirely by the recovery in crop yields.

In contrast, the outlook for the oil, gas, and mining sectors is not normalization but continued expansion. These activities have been steadily growing, leveraging Argentina's vast natural resources that are already being exploited. Unlike most other industries, which faced setbacks during the pandemic, the oil, gas, and mining sectors have maintained a steady growth from 2021 to 2024. In the case of upstream oil and gas, the development of Vaca Muerta is driving a surge in production, with domestic demand fully met and surplus output directed towards exports. Official forecasts suggest that by the end of the decade, Argentina could be exporting approximately $30 billion in energy, primarily crude oil, contributing around $25 billion to the trade balance.

Meanwhile, the downturn will not be evenly distributed throughout the year. The largest impact occurred in the first quarter, with a somewhat milder decline in the second quarter, followed by a gradual recovery. Since this is a demand-driven recession (unlike the supply-driven contraction caused by the pandemic lockdown), the recovery will be slow, driven by the gradual improvement in real incomes. With an almost 4.0% i.a. expected contraction in 2024, the economy will likely return to pre-recession levels by 2025.

Beyond this rebound, the success of the macroeconomic reforms—alongside microeconomic reforms aimed at getting deregulation, trade normalization, and labor market flexibility—will be crucial to retrace the productivity growth path Argentina failed to keep about 15 years ago.

- Inflation: Current rates and expectations

Argentina is one of the countries with the longest history of inflation globally. Since 1983, when democracy was restored, the average annual inflation rate has been 70.8%, excluding periods of hyperinflation. Overcoming this entrenched inflationary history is the real challenge, as it's impossible to make sound investment or consumption decisions when prices are constantly fluctuating.

However, inflation—along with rising public debt and currency volatility—are merely symptoms of a deeper issue: chronic fiscal imbalance. With this in mind, the current Administration has tackled inflation at its root, not by relying on monetary tricks, but through a strong fiscal anchor. This involves sharply reducing public spending, particularly in subsidies and discretionary expenses, and curbing the Central Bank’s role in financing deficits, aiming for a sustainable fiscal path.

During the first months of the Administration, significant progress was made in partially correcting distorted relative prices, including exchange rate, regulated prices, and public service tariffs. Improvements were introduced to streamline the payment flow for imports, reducing regulatory hurdles and implementing a new fiscal plan, with a strong focus on achieving financial balance and regaining market confidence.

However, the ongoing nominal race between prices and the exchange rate poses a substantial threat to the economic plan. The accumulated lag which has been observed since December raises concerns about the future path of inflation and economic activity, particularly if exchange rate adjustments are accelerated. This delicate balance imposes a temporary cap on price increases, potentially creating room for a future recovery in real incomes if managed effectively.

For 2024, based on market consensus, annual inflation is expected to be around 120% in December (assuming no further jumps in the exchange rate). This projection hinges on a near-complete adjustment of relative prices and a significant drop in core inflation, with monthly inflation expected to decelerate to approximately 3.5% by the last quarter of the year. However, the key to this slowdown—and a significant threat to the acceptance of the program by the society—lies in maintaining economic activity at a sustainable level.

- Currency Exchange Rates and International Reserves: Recent movements, Central Bank interventions

The recurring fiscal crises, coupled with increased monetary issuance and exchange rate volatility, have put significant pressure on Argentina’s external sector. The excess supply of pesos has driven an overwhelming demand for foreign assets, which has consistently consumed the entire current account surplus. To manage this, Argentina has frequently resorted to capital controls, which have been in place since 2019. These controls create a currency gap between the official and free market exchange rates, hindering growth and causing some distortions in the economy. Moreover, the external imbalance is depleting international reserves, which are now in negative territory. Without external financing, lifting currency controls is risky, but maintaining the current system is equally perilous. This is the central challenge the Argentine economy is facing today.

The current administration inherited a Central Bank with net negative reserves totaling USD -11.5 billion and monetary liabilities amounting to 11.3% of GDP. On the fiscal side, the national public sector was running a deficit of 5.0% of GDP, which had been largely financed through monetary issuance.

This situation led to a currency gap (between official and free market rates) that exceeded 150%, along with double-digit monthly inflation rates, culminating in an annual inflation rate of 211% by the end of 2023. Following the sharp 118% devaluation in December, the Government implemented a daily exchange rate adjustment, resulting in a 2.0% monthly depreciation.

While the real exchange rate initially had room to appreciate after the devaluation, the accelerating inflation has already eroded most of that "buffer." Although this gap was briefly leveraged, an increase in the disparity between exchange rates is unlikely to happen, and inflation will persist in the coming months.

The official real exchange rate is currently 45% below the one recorded in December 2019, and over the last 25 years, there have only been four instances when the real exchange rate was lower than it is now: the exit from convertibility, after the 2023 primary elections, at the start of the current government, and during the 2016-2017 period. During that time, relative stability was maintained without capital controls, supported by a generous supply of external financing, which sustained the exchange rate parity until it abruptly ended in April 2018. This highlights the significant lag the official exchange rate is experiencing today.

Despite the ongoing trade surplus, the Central Bank (BCRA) is finding it increasingly difficult to accumulate international reserves and escape the negative balance. This is partly because under the current "blend dollar" system (20% of export earnings are not settled through the official exchange market), while payments for imports continue to rise, reducing the "cash" trade surplus. Although the trade balance remains positive, it is shrinking. Additionally, the burden of real and financial service payments, along with foreign currency debt obligations, is putting further pressure on the balance of payments. As a result, the currency balance remains in deficit. Unless changes are made, this deficit is expected to worsen in the coming months, with the Central Bank solidifying its position as a net seller of foreign currency. Adding to this pressure are upcoming public sector debt repayments, which could further deepen the negative trend in net reserves.

Despite the clear deterioration of the balance of payments, the Government is torn between continuing to prioritize the short-term fight against inflation and moving towards exchange rate liberalization. While liberalization would undoubtedly have short-term effects, it would provide greater long-term sustainability to economic policy, allowing the country to benefit from deregulation and fiscal balance.

- Public Debt and Fiscal Deficit: Levels, trends, and implications for investors

As we have mentioned before, Argentina’s economic problems are mainly rooted in fiscal issues. Based on the fact that, in the last 60 years, only 6 have had a financial surplus, the country has historically relied on monetary issuance and public debt (expensive due to the history of recurring defaults) to finance imbalances. 2023 was not the exception, ending with a primary deficit of 2.7% of GDP and 3.3% after interest payments.

At the beginning of the new Administration, an adjustment of 5 percentage points of GDP was proposed and deemed sufficient for the economy to reach fiscal balance in the first year of the Government. According to the fiscal plan projected by the Government in the early days of the Administration, half of the adjustment came from a reduction in spending. The mainly impacted areas included public works, subsidies for public services, transfers to provinces, and public sector salaries, with social policy being the only component that saw an increase, serving as a tool to cushion the initial decline in incomes. The remaining adjustment was achieved through tax hikes, particularly the increase in the PAIS Tax, which is levied on foreign currency transactions and, at a higher rate, imports of goods.

The main threat this initial pillar faces is that it could become entangled in a negotiation process that weakens its effectiveness and prevents it from becoming fully implemented. Based on our projection, the fiscal adjustment for 2024 will likely bring the economy to an initial balance (before interest payments) rather than a full financial balance. While this would be a positive outcome, it would still leave the Government with financing needs equivalent to about 1.0% of GDP.

While the Government's primary focus has been on cleaning up the Central Bank's balance sheet, this effort has increased Treasury debt, posing a latent risk to the broader economic program due to the challenging short-term debt maturity profile. In July alone, the total public debt stock rose by USD 9.6 billion, reaching USD 452 billion, equivalent to 74% of GDP—10 percentage points higher than in November 2023. Domestic debt now accounts for 44% of the total (up from 38% prior to the currency depreciation in December), with only a third of it at a fixed rate. The remaining two-thirds are indexed either to inflation or, to a lesser extent, to the exchange rate.

Compared to a year ago, public debt increased by USD 46.5 billion (+11.5%), driven entirely by local currency debt, which, when valued at the official exchange rate, rose from USD 143.95 billion to USD 195.7 billion (+11% y/y). Within this category, inflation-linked debt (adjusted by CER) saw the most significant increase, jumping from USD 77.3 billion to USD 133 billion. Meanwhile, foreign currency debt decreased by USD 5.2 billion, bringing the total down to USD 254 billion, despite an increase of USD 3.3 billion in debt owed to the IMF. This decline was largely attributed to the repayment of bonds and obligations to other international organizations.

3. Political Landscape and Risks

- Overview of the current Government and its economic policies

One of the key challenges the current Administration is facing lies in the political feasibility of implementing structural reforms. The ruling party holds only 38 seats in the Chamber of Deputies and 8 in the Senate, representing about 15% and 11% of the total seats, respectively. With such a limited representation, pushing forward reforms that require legislative approval has proven difficult.

As a result, the national Government has resorted to using emergency executive orders and vetoing legislation, tools that could eventually face legislative resistance. This approach underscores the need to strengthen political negotiations and maintain popular support to sustain the Government's reform agenda.

However, this formal political weakness is offset by the informal power that Milei enjoys, especially during the early months of his presidency, when high expectations are still in place. Despite significant economic adjustments and inflationary pressures, the Government Confidence Index, adjusted for economic perception, reached a record high in December 2023, the highest since the measure began in December 2021. As of August 2024, it remains at very high levels, more than 45% above the average.

Inflation reduction stands as the Government's strongest asset in maintaining public support. This is likely why the short-term inflation reduction has become the Administration's main political and economic priority, even when other potential challenges within the economic plan are emerging. To maintain public approval, the Government has postponed some relative price adjustments, ensuring they do not heavily impact on the monthly inflation index (CPI), while continuing the policy of a 2.0% monthly currency devaluation.

Ironically, this intense focus on curbing inflation in the very short term poses the greatest threat to the economic plan. The delay in currency adjustment is beginning to fuel demand for foreign goods and services. Should this result in a devaluation of the exchange rate by the last quarter of the year (without lifting foreign exchange controls), it could trigger another inflation spike, raising serious questions about continued public support, which will be crucial in the 2025 legislative elections, when the Government will need to strengthen its presence in the National Congress.

- Structural economic reforms ongoing

In Argentina, no private-sector jobs have been created in the last 12 years. As public employment is financed with taxes, it cannot substitute private employment. No social program will be sustainable if it fails to generate private sector jobs. Likewise, no economic program will be sustainable without sustained growth in exports. The main constraint is internal, rather than external: it’s not that Argentina lacks the capacity to generate foreign currency, but rather that it fails to retain it voluntarily, leading to currency controls that further fuel distrust.

Due to this, and in addition to the macroeconomic stabilization plan, Argentina needs structural economic reforms to retrace a growth path. The country requires a “new economic architecture” with modern, sustainable, and predictable rules. Key reforms include labor market adjustments, deregulation efforts, and higher public-sector efficiency. While these measures aim to enhance long-term growth prospects, their success will depend on overcoming significant social and political resistance.

The new Administration introduced an Emergency Executive Order (DNU), a regulatory tool that allows the Executive Branch to make changes with the force of law unless Congress secures the majorities required to overturn it. This DNU eliminated controls on some of the central prices of the economy, marking an important step forward towards economic reform.

In addition, the National Congress passed the so-called 'Ley Bases,' which includes significant structural reforms. These reforms feature labor changes that extend the trial period and reduce hiring penalties (which had been more of a barrier to entering the labor market than to leaving it), privatizations and concessions of state-owned companies, the repeal of the pension moratorium, tax adjustments, and the dissolution of public agencies, interventions, and trust funds. Additionally, there is progress on an economic deregulation agenda that will increase competition in sectors such as aviation, while easing trade regulations that had previously imposed high costs on imports.

4. Scenario Analysis and Forecast

Based on the August 2024 market expectations survey (Central Bank’s "Relevamiento de Expectativas de Mercado"), projections for 2025 indicate a more stable outlook compared to 2024, with expectations of moderating inflation, a recovering economy, and a stronger fiscal position.

After the expected contraction of around 3.8% in 2024, the economy is projected to grow by 3.5% in 2025. This growth is anticipated as part of a rebound driven by improving economic conditions and recovery efforts in key sectors such as agriculture and industry.

For 2024, the median forecast suggests an annual inflation rate of 122.9%. However, inflation is expected to moderate significantly in 2025, with projections placing annual inflation at 38.4% by the end of that year.

By December 2024, the exchange rate is projected to reach $1,025.4 per USD, reflecting a real appreciation of the peso. The Argentine peso is expected to continue depreciating in nominal terms in 2025, with the median forecast predicting that the exchange rate will reach $1,514.6 per USD by December 2025.

A primary fiscal surplus of $7.8 trillion is expected for 2024, an improvement from previous forecasts. For 2025, a larger primary surplus of $10.5 trillion is anticipated, driven by fiscal adjustment measures aimed at enhancing fiscal responsibility and reducing deficit levels.

As previously mentioned, the main risks lie on the external front. A potential change in exchange rate policies or a sharp devaluation could lead to an upward deviation in inflation, although it may also result in better economic recovery.

5. Alert and Opportunity Dashboard

.avif)