ARS-DENOMINATED STRATEGIES

External dynamics continue to raise red flags. As discussed in Confidence or Correction: The External Front Dilemma, with the current account once again in deficit, the challenge lies less in the size of the imbalance and more in its financing. Should market access consolidate –as suggested by the issuance of the Bonte 2030, the first international peso-denominated placement since 2018– the exchange rate could remain stable around current levels; otherwise, the adjustment would likely fall on the exchange rate or real activity. In this scenario, external pressures on FX keep carry trade strategies on alert, strategies that had been gaining traction amid a relatively stable exchange rate trading below the center of the band. Still, an inflation print around 2% –or even lower– could give fresh momentum to the fixed-rate peso curve.

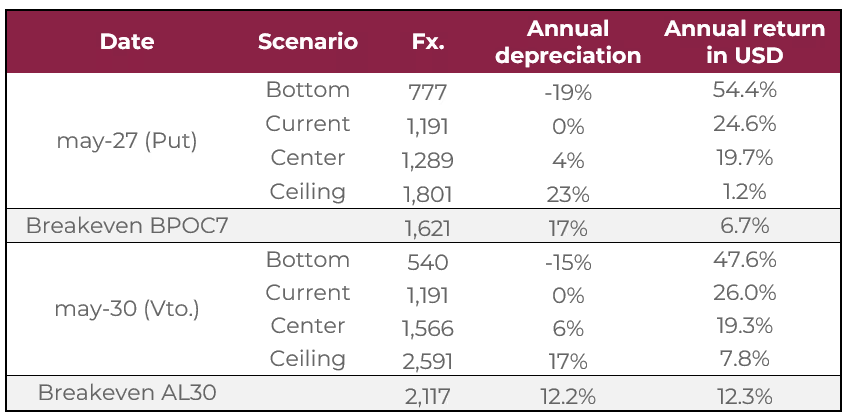

The Bonte 2030 was issued at a nominal annual rate of 29.5%, a high yield that reflects the perceived FX risk among investors. When priced to the May 2027 put date, this rate implied a dollar yield of 6.3%, even assuming the exchange rate moved to the top of the band. If valued to maturity, the annualized dollar return rose to 12.5% under that same scenario. However, compression in the secondary market –with the TY30P trading at 26.9% as of June 26– suggests there may be room for future placements at more competitive rates. Even so, while the implied depreciation against the AL30 narrowed –from 17.4% annually at issuance to 12.7% currently– the market still anticipates an exchange rate above the center of the bands by 2030.

In this context, the carry trade still holds some short-term appeal, but its potential is gradually diminishing as conditions tighten. A stable exchange rate and the May inflation print of 1.5% –reinforcing a disinflationary path that continues to consolidate– could support the fixed-rate curve, sustaining interest in these positions. However, their sustainability hinges on the absence of renewed exchange rate pressures. The recent Bonte issuance reflected some appetite for peso risk, though investors still demand a significant premium amid prevailing uncertainty. With a current account in deficit and expectations of a higher exchange rate over the medium term, the risks surrounding these strategies remain present.

That said, for investors with a higher risk tolerance, we continue to favor the short end of the fixed-rate curve for carry trade strategies. In particular, we highlight the S29G5 and S30S5, which yield 2.5% and 2.3% effective monthly rate (TEM), respectively, with breakeven exchange rates around ARS 1,275 and ARS 1,301. However, we caution that the performance of these strategies remains highly dependent on external sector dynamics. Despite strong agricultural FX inflows –USD 825 million recorded last week– demand for foreign currency remains firm, keeping pressure on the exchange rate even during a seasonally favorable period for the sector and while the temporary suspension of export taxes remains in effect through the end of June.

For more conservative profiles, the 2026 segment of the CER-linked curve continues to offer attractive value for 3- to 6-month horizons. Even under a scenario of sustained disinflation, these instruments provide a potentially higher return than fixed-rate alternatives. Current pricing already reflects relatively elevated real rates, in a context where expected inflation over the coming months could moderate more quickly than nominal rates. This backdrop strengthens the case for medium-term positioning in CER-linked bonds, particularly via the TZXM6 (CER +12.4%). While effective returns will depend on the exit yield at the time of unwinding, the breakeven yield on the 2026 segment stands at around 14.6% over six months compared to fixed-rate instruments, implying a potential spread compression of up to 460 basis points.

For longer-term strategies, we suggest the dual bond TTM26. The average breakeven TAMAR rate stands at 23.7%; in other words, for the TTM26 to pay the floating leg instead of the fixed rate at maturity, the projected average TAMAR from now until then would need to exceed that threshold. Although our projections anticipate a decline in nominal rates, the average wholesale rate would stand above the current breakeven. At current levels, the floating leg offers a direct yield of 29.7%, considerably higher than the direct yield of 22% offered by the T13F6.

Recommendation: for peso-denominated investments, we suggest the following portfolio allocation: 10% S29G5 (2.7% EMR) + 10% S30S5 (2.6% EMR) + 30% TZXM6 (CER +12.4%) + 30% TZX26 (CER +12.3%) + 20% TTM26 (2.35% EMR or a spread of 4.5% NAR over wholesale rate).

DOLLAR-DENOMINATED STRATEGIES

So far in 2025, Argentina’s sovereign bonds in dollars have outperformed those of comparable countries. While the latter show an average increase of 0.4%, the Argent and Bonar bonds have accumulated a 2.2% YTD gain, despite the rise in U.S. Treasury yields.

In this context, we maintain a constructive long-term view on dollar-denominated fixed-income assets, aligned with the possibility of a political scenario favorable to LLA in the upcoming elections. Such an outcome could help consolidate a more predictable macroeconomic environment. This, in turn, would enable further compression of sovereign risk and bring Argentina closer to regaining access to international debt markets –a key factor to sustain a current account deficit with less pressure on the exchange rate or economic activity.

In the short term, however, the performance of sovereign hard-dollar debt could show some sideways movement. This is partly due to the government’s decision not to intervene in the FX market within the floating bands, which limits reserve accumulation –still a critical variable for assessing financial sustainability and market access conditions. While the Treasury has chosen to build reserves through debt issuances, such as the Bonte 2030 –which would contribute USD 1 billion on a monthly basis–, these efforts have yet to translate into a consistent improvement in bond performance.

In this context, the ARGENT 35 and ARGENT 41 stand out as the bonds with the highest upside potential within the sovereign curve, both offering yields around 11%. Assuming a sovereign risk compression scenario toward levels below 500 bps over a 12-month horizon, the ARGENT 35 offers a potential return of 21.8%, while the ARGENT 41 could reach 25.3%.

Given the possibility of sideways price movements in the sovereign curve, we believe it is appropriate to partially diversify into BOPREAL. These instruments have shown lower volatility during periods of political uncertainty, such as the months leading up to elections, and have delivered a 7.5% YTD gain. Within this asset class, the BOPREAL Series 1-C stands out with a yield of 8.8%, above the rest of the instruments in the same series.

For more conservative profiles, we recommend positioning in long-dated corporate bonds in dollars under New York law. These assets combine higher yields with lower exposure to local volatility, while also offering greater liquidity and trading depth, providing investors with more flexibility. We highlight the YPF 2031 (YMCUO) with a 7.5% yield, Telecom 2031 (TLCMO) with an 8.7% yield, and TGS 2031 (TSC3O) with a 7.4% yield.